In a world of unpredictable yet unavoidable change, individuals, companies and even governments turn to the insurance sector to be prepared. Insurance needs are changing in many ways, such as including risks related to climate change like floods or bushfires, or even novelties like ‘hole-in-one’ insurance (where a golf tournament insures itself to pay the prize bonanza on the off chance that a hole-in-one is achieved). With an increasingly online generation, even as traditional insurers bank on the credibility and trust they have accumulated, the new age InsurTech companies chip away at the market with digital experiences and new models.

When it comes to innovating with technology, InsurTech companies have an advantage over traditional insurers. They are nimble and flexible with their offerings, able to quickly establish low-cost digital platforms and new operating models. InsurTech companies’ biggest advantage is the hold they have over the customer’s pulse. With smartphones becoming commonplace, customers find that InsurTech offers comfort, convenience, and speed in making important insurance-related decisions and transactions.

Research indicates that 28 of the 280 FinTech firms that have turned unicorns to date have played an instrumental role in driving innovation or disrupting the way insurance is done. From claim management to reinsurance, asset management, customer onboarding, and engagement, InsurTechs have earned their colors across the insurance value chain and are here to stay.

Challenges to InsurTech

Despite these gains, experts believe that InsurTech market growth will have to endure several constraints. Foremost among them is a lack of awareness about the value InsurTech can deliver, and dearth of professionals who can expertly work with advanced technologies. These factors could restrict InsurTech companies from scaling their technology capabilities to the extent desired.

However, it is undisputed that the future of insurance will be tech-driven in the form of embedded ecosystems, AI & ML, blockchain, low code technology, and more. 85% of insurance companies recognize the need to prioritize digitalization, so it may not be long before traditional market leaders catch up with their technology capabilities or look to buy out smaller players. InsurTech start-ups have their work cut out in gaining the kind of trust and credibility enjoyed by established insurers. Now, they must rethink strategy to retain their technology advantage.

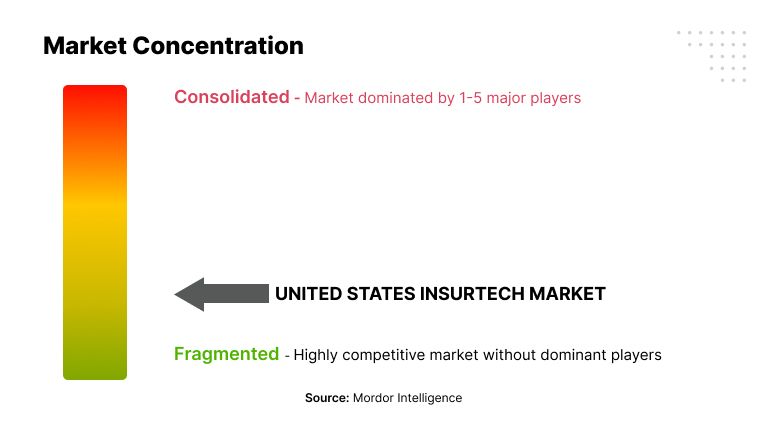

If we look at the US which is the global market leader, InsurTech is expected to grow at more than 7% CAGR over the next five years. The competition is definitely heating up here.

Read more: The Rise of FinTech in Asia: Success Stories and Learnings

Business opportunities for insurance will continue to flow in as the world becomes increasingly digital. More aspects such as health, travel, auto, and home will be included under the umbrella of online insurance.

InsurTech companies will need rely on their strength – technology – to offer a wider, more personalized range of benefits shaped by data, new offerings like social insurance, and cost saving tools like virtual agents powered by conversational AI etc.

McKinsey research opines that five rapidly advancing technologies will significantly redefine the future of insurance. These include applied AI, distributed infrastructure, future of connectivity, next-level automation, and trust architecture. By putting the full force of their tech advantage here, InsurTech players can solidify their business and expand their portfolio.

1. Powering up core processes with AI

Since the pandemic, at least a quarter of life insurers in the US have expanded their automated underwriting practice to simplify the application process. From reducing claims processing time and cost to improving fraudulent claim detection and claim adjustment processes, AI and automation are proving be invaluable.

Take for example, the AI-enabled platform offered by Bdeo, available on their mobile app. It comes with a chatbot that uses Natural Language Processing principles to liaise with claimants, get first-hand info on the accident/damage that has occurred and helps them share photographic evidence of acceptable quality on the platform. The insurer can use the app to inspect and investigate the incident remotely using computer vision models. Doing so helps avert errors in evaluation and improves the overall claim processing experience for both the insurer and claimant.

Studies predict that AI will disrupt underwriting, claims, marketing, distribution and other core processes by enabling more human-like interactions across various customer touchpoints. There is a plethora of opportunities that can be exploited. For example, the associated customer data can be used for predictive analysis and forecasting, which can in turn, inform the development of new product and service lines.

2. Enabling intelligent insurance with distributed infrastructure on the cloud

Many core insurance processes that have been weighed down by legacy systems are finally modernizing. This allows insurers to leverage cloud-native infrastructure, ramp up to manage workloads without impacting customer experience and speed up their innovation efforts. Thanks to cloud computing, they will be better placed to harness the massive amounts of claim-related data available to benefit their customers and increase profitability.

This is a huge opportunity for traditional insurers to collaborate with InsurTech to form partnerships that leverage their strengths and quickly enable plug-ins, distribution channels, and other value-adds. For instance, InsurTechs can offer digital solutions to efficiently sift through vast historical data of established insurers, to identify and interpret customer patterns and insights to determine the kind of new product/service lines to be developed. In fact, at least 75% of insurers were found to be seeking out InsurTech collaboration to improve their customer experiences according to a Capgemini survey.

3. Developing insurance products using telematics

Telematics technology is increasingly being used to monitor, interpret, even influence consumer behavior. For example, innovation stimulated by IoT adoption is being applied in connected home devices to track humidity, temperature and other parameters, which potentially cause damage to property. Insurers can leverage the data generated on these devices to estimate risk over time. Similar innovations are being explored across the domains of insurance to life, health, auto, manufacturing, commerce etc. The advent of 5G will enable real-time data sharing and make it possible for insurers to turnaround services faster than ever.

For example, being covered against ride cancellations is a value-add for customers and digital solutions can be developed to enable this as a timely service using real-time availability of data. Another example of value-add is the coverage against bodily harm to earners and riders of every trip offered by Uber in partnership with a leading insurer.

4. Enabling human decisions via bots

While robotic process automation (RPA) has proved its worth in automating back-office functions in the insurance industry, there’s a lot it can do in terms of next-level process automation that will shape the future of insurance. For example, the IoT-enabled, real-time monitoring of factory equipment can predict maintenance needs and prevent repair or damage that result in insurance claims.

RPA also has a distinct role to play in supporting human decisions in a cost-effective and timely manner. As an example, it can expedite claims processing wherein photos of the damage to a vehicle are automatically assessed and verified for authenticity without requiring an in-person visit by a claims adjuster to the damage site. Likewise, building optical character recognition features into RPA will help extract text from claim applications in large volumes and ensure that the information it contains is distributed to the right functions for further processing.

5. Laying the foundations for trust with blockchain

Increased digitalization of insurance is raising security concerns due to the sensitive nature of customer data that is being shared across the insurance ecosystem. Building customer trust will be a priority for insurance players, which is where blockchain comes to the rescue.

Along with its advantages of transparency and efficiency, blockchain will play a leading role in helping carriers safeguard customer data from cyberattacks and data breaches. It will also simplify user authentication, identity management, and fraudulent claim detection etc. Through blockchain-based smart contracts, policies can be converted to decentralized lines of codes that will make consumer’s data immutable and easily available for immediate verification in the event of any claims made to the insurer. If it proves to be fraudulent, the contract will immediately be discontinued, and the premium amount paid returned to the insured. This kind of data transparency and responsiveness of the system will help build trust between all concerned parties.

The future of digital insurance paved by tech-led design

As insurance becomes more digitally driven, user experience (UX) will be all the more crucial for branding. While an omnichannel insurance experience is the norm today, creating memorable user experiences at all possible touchpoints will be paramount to carving out stronger market positions for the InsurTech brand.

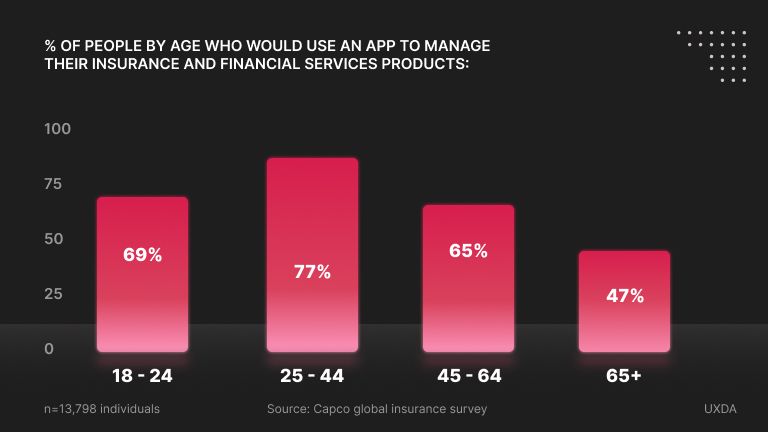

For example, the silver agers generation are no longer the most dominant consumers of insurance. In fact, studies that the interest now being shown by millennials and Gen-Zers towards insurance products exceeds that of the older generations.

Or, as this chart indicates, nearly half the individuals in the 65+ age category are unlikely to use an insurance app. If the insurer wants to attract more consumers from this cohort, they will need to leverage data to understand preferences, simplify interfaces, customize their offerings and so on.

According to the World InsurTech Report 2021, half of the insurance customers are willing to explore solutions offered by new-age digital players. The insurance market will experience disruption and a new order will emerge. Traditional insurers are more likely than ever to engage in partnerships with InsurTechs to stay relevant. Niche players and start-ups in InsurTech will not only need to leverage emerging technologies but also understand the complexities of insurance better and closely follow changing needs of their target demographics.

Led by research, data analytics, and empathic and intuitive design of user-centric interfaces, InsurTech players will be able to create market differentiation that can help them explore opportunities to build partnerships with traditional players so that both survive and thrive.